How to Get a Personal Loan With No Income Verification

It's possible to get a personal loan without income verification, but it may not be a good idea

There are ways to get a personal loan without needing an income verification, such as by having a sufficiently high credit score. However, these no-income loans can be more expensive and riskier than traditional options. So it’s important to consider the pros and cons—and perhaps look at other financing options—before deciding.

Key Takeaways

- No-income loans exist, but they're fairly risky.

- Your credit score and assets can impact your personal loan options.

- Alternatives to no-income loans include HELOCs, co-signed loans, and withdrawals from retirement accounts.

What Is a No-Income Loan?

Unlike home loans and other forms of secured lending, personal loans tend to be unsecured, meaning they generally don’t require collateral or a repayment guarantee. Instead, lenders typically analyze your earning capacity and credit history to determine whether you qualify for a personal loan.

People who aren’t earning enough, have no current income, or have poor credit scores generally don’t qualify for personal loans. So, they may have to seek out other forms of borrowing that come with no income verification.

Even though these types of loans don’t require traditional incomes, you typically still need to provide proof of some form of an income source, such as:

- Dividends and interest

- Social Security

- Unemployment

- Alimony

- Child support

- Pension or annuity income

Types of Loans That Don’t Require Income Verification

Here are some common types of no-income loans to consider:

Personal Loans for Excellent Credit

People with excellent credit scores (in the range of 740 to 850) and a strong credit history may qualify for personal loans without showing proof of ongoing income. For example, lenders like Upgrade and Universal Credit don’t have minimum income requirements and offer loans based on credit history.

Tip

Borrowers with high credit scores can receive lower interest rates compared to those with lower scores.

Secured Loans

Secured loans require collateral to ensure the lenders can recover the money if you delay or fail to make repayments. Here, you can use any asset as a guarantee, like your house, car, or precious jewelry. In case of non-payment, the lender can seize these assets, making it a highly risky option.

Pawnshop Loans

If you urgently need cash, you can give a valuable item to a local pawnshop in exchange for a small loan. The item will be held until you can pay the money back. If you’re unable to repay the loan, the pawn shop can choose to sell off the item to recoup the costs.

Pawnshops can be highly regulated with loan maximums and interest rate caps set by the state they’re in. For example:

- Alaska: Max loan amount is $750 with interest capped at 20% per 30 days.

- Florida: Interest capped at 25% per 30 days.

- Nevada: Interest capped at 13% per month with a $5 initial fee.

While pawnshop loans don’t look at a person’s income or credit score, they typically charge high interest rates and may require additional charges like storage fees, making it a more expensive option than other forms of borrowing.

However, they can be convenient when you’re in need of cash without having the time to go through a bunch of paperwork and approvals.

Cash Advances

Cash advances are short-term, unsecured loans that can get cash in your hands quickly but typically come with very high interest rates and additional fees. They can be accessed through your existing credit card provider and will appear as a charge on your credit card, or you can get them through online cash advance apps like Varo, Brigit, and Payactiv.

Typically, cash advances need to be repaid quickly within a few days or when you receive your next paycheck.

Payday Loans

As the name suggests, these loans let you borrow a small amount of money that must be paid back on your next payday. These are typically limited to $500 but come with extreme interest rates and additional fees, which can worsen your financial crunch.

Important

Some workplaces offer cash advances and payday loans, so you can receive a part of your salary in advance and the amount with interest will automatically be deducted from your next paycheck.

Disadvantages and Potential Risks

While no-income loans can be useful for those not qualifying for traditional forms of personal loans, they come with a host of disadvantages and risks to consider before signing up for one.

High Interest Rates and Fees

Since no-income loans don’t use collateral or consider your credit history, they need to rely on other measures to ensure they can recoup their investment. That’s why they tend to carry much higher interest rates and additional fees compared to traditional personal loans. For example, the interest rates and fees on car title loans can come with an APR of 300%.

Short Repayment Terms

Some no-income loans like cash advances and payday loans tend to have very short repayment times like 30 days or until the date of your next paycheck. These can make it difficult to arrange the repayment money, especially considering the higher interest rates and fees that worsen your financial problems.

Cycle of Debt

As no-income loans can be difficult to repay on time, some borrowers seek new loans to pay off existing ones, creating a cycle of debt. It can become difficult to keep up as interest rates and fees add up over time.

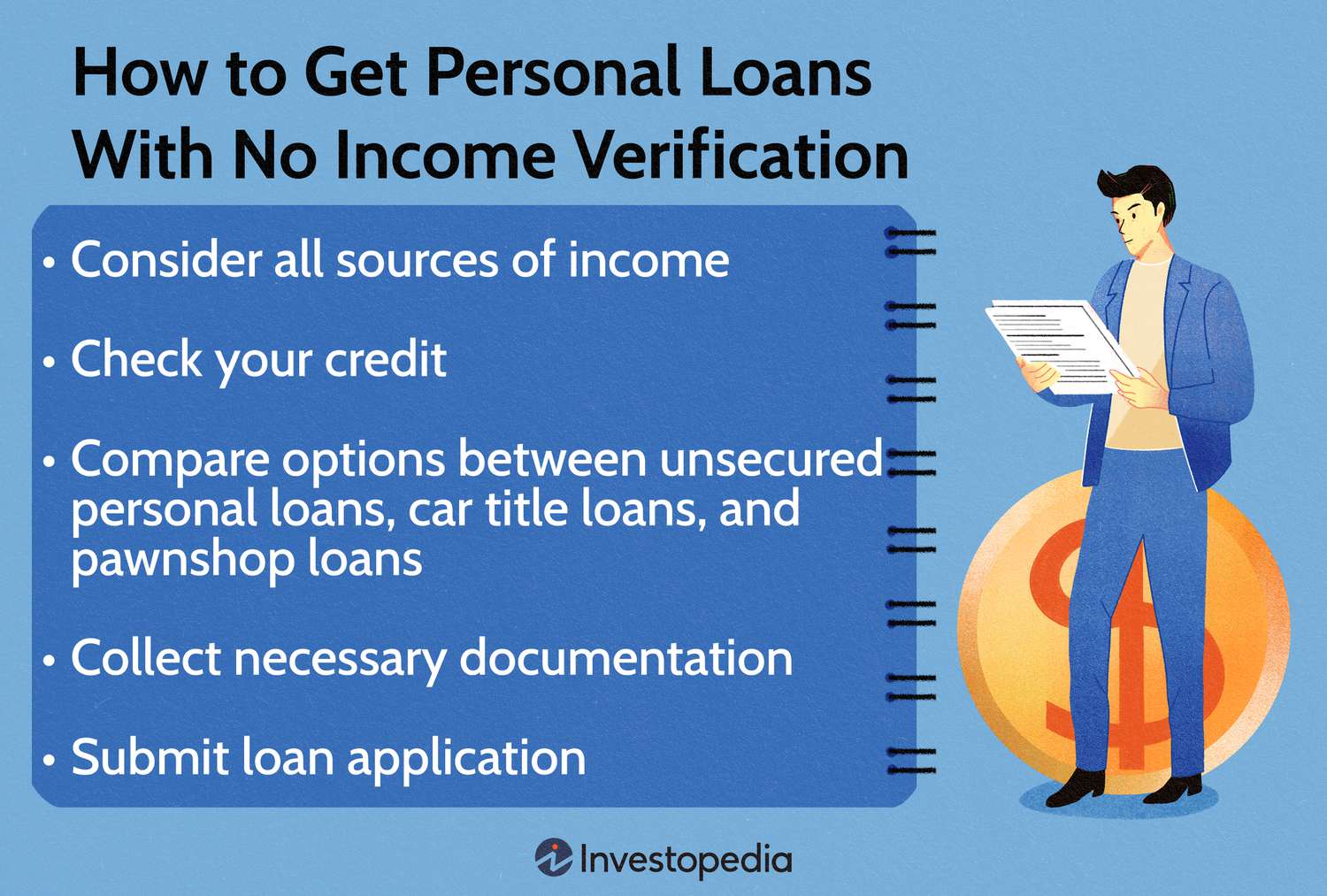

How to Get a Personal Loan With No Income Verification

- Consider all income sources: Even if you don’t have a typical income, consider other sources of money like Social Security benefits, alimony, and worker’s compensation payments that can help you qualify for loans.

- Check your credit score: People with no current income but with a high credit score may qualify for personal loans, so check your credit reports and review your creditworthiness before opting for riskier, high-interest options.

- Compare options: Consider different loan options and evaluate their pros and cons, analyzing your current financial situation. You may find other loan options more feasible than risky unsecured loans.

- Collect relevant documents: Most loan applications will require some form of documentation, especially your identity verification, proof of ownership for assets, and credit history reports.

- Apply: Depending on your lender, you can apply online through a digital form, but some lenders, like pawnshops, may require in-person visits and verification.

Alternatives to No-Income Loans

Before committing to no-income loans—which often come with high interest rates, short repayment periods, and the risk of falling into debt—it’s worth exploring other options that might be more affordable and less risky.

Home Equity Loan or Line of Credit

Homeowners may be able to borrow against home equity. These options typically offer lower interest rates than no-income personal loans as they’re secured by your home. However, missing payments can result in foreclosure, making this a risky option if you’re unsure about repayment.

Loan or Withdrawal From a Retirement Account

If you have a 401(k), IRA, or another retirement savings account, you might be able to take out a loan or early withdrawal. Certain situations, such as medical expenses, may allow you to withdraw money from an IRA without penalties.

Co-Signed Loan

If you don’t qualify for a personal loan but you know someone who does, you may consider applying for a loan together, as a co-signer. By co-signing the loan, you family member or friend could act as a guarantor, taking on the responsibility for making payments if you can’t.

Warning

These loans will appear on the co-signer’s credit reports and missed payments can lower their credit score.

Credit Union Emergency Loan

Some credit unions offer small loans to cover emergency expenses like unexpected medical bills. They typically offer lower interest rates than other quick-cash options like payday loans.

Tip

Use the National Credit Union Administration (NCUA’s) online locator tool to find a local credit union near you.

Loan or Grant From a Non-Profit Organization

Several non-profit organizations have low-cost loan and grant programs for people experiencing financial hardship. For example:

- Jewish Free Loan Association (JFLA): Provides interest-free emergency loans to cover essential expenses like rent, medical bills, and car repairs.

- HFLA of Northeast Ohio: Offers interest-free loans for unexpected costs such as funeral expenses, home repairs, or job loss.

- Modest Needs: Provides grants to help cover emergency expenses. These grants are technically not loans, so you don’t have to pay the money back.

Note

You can call 211, a free service that connects people to local financial assistance programs.

Credit Card

In urgent situations, using a credit card might be a better option than taking out a no-income loan, especially if your credit card has a low interest rate or offers an introductory 0% APR period.

Loan From Family or Friends

The safest and most flexible option might be to ask your friends and family for a loan. They can skip any interest charges and fees, while letting you pay the money back as and when you can, helping you avoid most of the risks that come with no-income loans.

However, be careful not to damage the relationship by taking the transaction lightly, neglecting repayment, and repeatedly borrowing without paying off the first amount.

The Bottom Line

Getting a personal loan without income verification is possible, but it’s rarely the best option. Many of these loans come with high interest rates and extra costs, short repayment terms, and serious risks. If you must take out a no-income loan, make sure to compare lenders, read the fine print, and have a clear plan for repayment to avoid falling into a cycle of debt.